For many working individuals, they can end up with different kinds of pensions over the course of their working life, including “defined benefit” whereby they are promised a certain level of pension from a certain age. Another is “defined contribution”, which is more common these days, and sees the only constant as the contributions from the employer.

With the above in mind, questions around pension consolidation arise.

To find out if you can benefit from pension consolidation, we have put together a blog that outlines the benefits and downfalls and explains why you need the help of pension transfer specialists.

What is a defined benefit pension?

Defined benefit pensions are pension plans whereby an employer or sponsor provides a specified pension payment, lump sum, or combination of both, on retirement. This amount is predetermined by a formula that is based on the employee’s earning history, length of service, and age.

What is a defined contribution pension?

Defined contribution pensions are a type of retirement plan whereby either the employer, the employee or both parties, make contributions on a regular basis. Benefits associated with defined contribution pensions are based on amounts credited to these accounts, plus investment earnings.

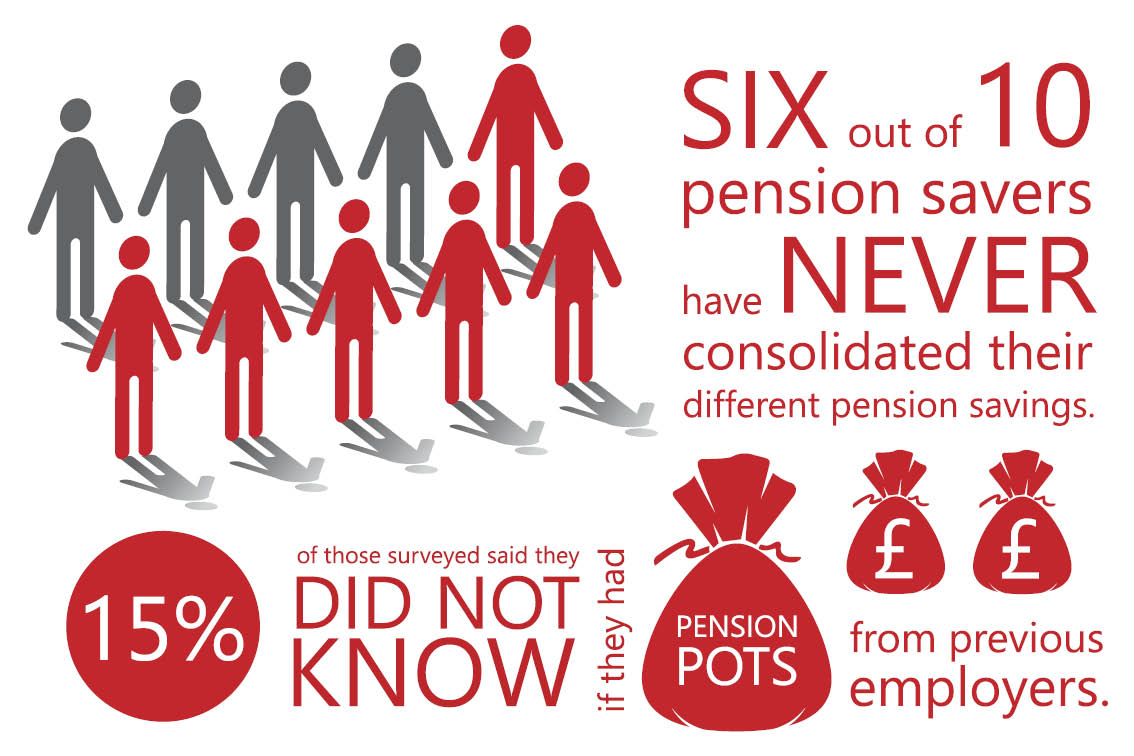

Can I consolidate my pensions?

It’s important to be aware that not all pension types should be transferred – you should consider and review the feature, benefits, and plan(s) of the pensions you are considering transferring and consolidating before making any kind of formal decision.

A pension transfer specialist can assist you with this, working closely to review your different pensions and providing guidance and advice on whether or not the pensions you have can be successfully and effectively consolidated or not.

What are the benefits of consolidating your pensions?

There are many benefits associated with pension consolidation. For example:

1. Improved investment performance

Some pension types have better advantages than others, and so by consolidating your pensions, you can remove the poorly performing pensions and welcome in consolidated investment performance, which plays a big factor into the pension income you will eventually receive.

2. Reduced charges

Some pension providers may take a fee from your pension for the services they provide, with this fee varying between different providers. By consolidating, you may reduce the amount of higher charging plans, typically the older plans, and enjoy getting more out of your pension.

3. Improved ease and quality of life

Having all your pensions consolidated in one place can reduce the complication and time-consuming stress of managing multiple unconnected pensions at once. For retirees with multiple pensions, it can be difficult to work out expected income, therefore consolidating pensions can make it much easier for you to manage both performance and contributions.

What are the cons of consolidating your pensions?

As with any kind of wealth transfer, there are some things you need to keep in mind, such as:

1. Investment detriment

In some cases, when a pension is invested in a ‘With Profits’ fund, market value reduction may be applied. While the reduction is relatively small, it is still something you should consider when looking to consolidate your pensions.

2. Exit penalties

While the majority of pensions can be merged without facing any fees or charges, there are some that may have exit fees applied to them. In this instance, you will need to pay a fixed amount for the consolidation of your pensions. In more cases than not, the small financial implication is worth it for the final result of a fully consolidated pension.

3. Complications of consolidating

The majority of individuals looking to consolidate their pensions are of retirement or pensioner age and can find the process of pension consolidation complicated and overwhelming.

Luckily, help is available to handle the consolidation process on your behalf, ensuring you get the most out of your newly consolidated pension.

4. Potential loss of benefits from other pensions

You may have pensions with existing benefits that are of use to you. In some examples of pension benefits, you may have the allowance of a tax-free lump sum that exceeds the usual 25%. Pensions such as these can be extremely valuable, and so you should consider these benefits before transferring.

Advice with pension consolidation UK

With many years of wealth management behind the business, I can support individuals with their pension consolidation as well as providing DB pension transfer advice.

To find out more about the pension consolidation services available at Michael Reed Wealth Management, please get in touch today.